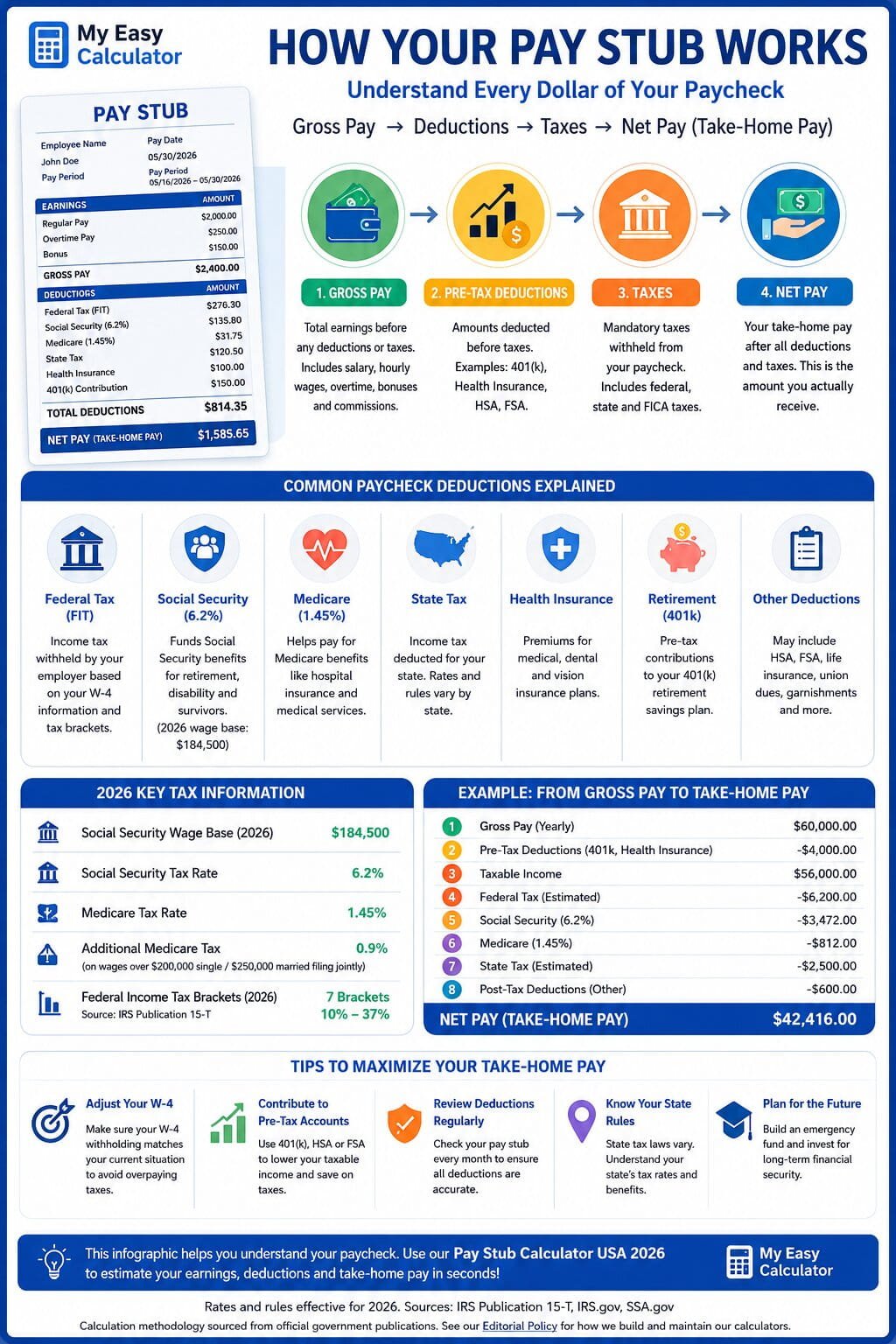

Pay Stub Calculator USA 2026: Calculate Net Pay, Payroll Taxes and Deductions

Use this pay stub calculator USA 2026 to estimate take-home pay from gross pay, hourly wages, overtime, federal income tax withholding, Social Security, Medicare, Additional Medicare Tax, state tax, local tax, and paycheck deductions. Enter your pay details, W-4 information, deduction amounts, and year-to-date wages to create a clear paycheck estimate for 2026 payroll planning.

What Is a Pay Stub Calculator?

A pay stub calculator is a paycheck estimator that converts gross pay into net pay by subtracting payroll taxes and deductions. Gross pay is the amount earned before deductions. Net pay, also called take-home pay, is the amount left after federal withholding, employee FICA tax, state and local estimates, pre-tax deductions, and post-tax deductions are applied. A good paystub calculator should not only show a final number. It should also explain the paycheck breakdown so employees can understand each line on a pay statement.

This USA pay stub calculator for 2026 is designed for the way modern payroll works. Federal income tax withholding is affected by pay frequency, filing status, Form W-4 Step 2, annual dependent credits, other income, deductions, and extra withholding. That means two workers with the same annual salary can have different take-home pay if their W-4 entries, benefits, or pay schedules are different. A weekly paycheck calculator, biweekly paycheck calculator, semi-monthly paycheck calculator, and monthly paycheck calculator can also show different per-check withholding because the IRS method annualizes wages before converting withholding back to the pay period.

The calculator also supports year-to-date wage entries because 2026 Social Security tax has an annual wage base, while Medicare tax has no wage cap. If your wages are near the Social Security limit, a basic gross to net pay calculator can overstate Social Security withholding unless it accounts for prior wages paid during the year. High earners also need Medicare tracking because employers must withhold Additional Medicare Tax after wages paid by that employer exceed the federal threshold. For state and local taxes, this tool uses custom percentage fields so employees can add a practical estimate for their location.

In simple terms, a pay stub calculator answers one question: how much of my paycheck will I actually receive after taxes and deductions? It is useful before payday, after a job offer, during W-4 updates, when adding a 401(k) contribution, when comparing overtime, and when checking whether a paycheck looks reasonable.

Who Should Use This?

This free paycheck calculator is useful for employees, hourly workers, salaried workers, job seekers, payroll admins, small business owners, and anyone who wants a quick 2026 net pay estimate. It is especially helpful when your paycheck includes overtime, pre-tax deductions, post-tax deductions, state withholding, local withholding, or W-4 changes. It can also help explain why net pay is lower than gross pay and why two paychecks with the same gross amount may not always produce the same take-home amount.

- W-2 employees checking whether their pay stub deductions look reasonable.

- Hourly workers estimating regular pay, overtime pay, and final take-home pay.

- Salaried employees comparing weekly, biweekly, semi-monthly, and monthly pay.

- New hires comparing job offers by net pay instead of gross salary only.

- Employees changing Form W-4 after marriage, dependents, side income, or a second job.

- Workers adding 401(k), HSA, FSA, health insurance, or other payroll deductions.

- High earners near the 2026 Social Security wage base or Additional Medicare threshold.

- Payroll and HR teams needing a simple explanation tool for paycheck questions.

- Small employers checking a rough payroll estimate before using formal payroll software.

- Budget planners who need a take-home pay calculator USA result before setting monthly spending.

How to Use the Pay Stub Calculator

- Choose the pay type. Select gross pay per paycheck if you already know your pay before deductions. Select hourly pay if you want the hourly paycheck calculator to create gross pay from hourly rate, regular hours, overtime hours, and overtime multiplier.

- Select pay frequency. Choose weekly, biweekly, semi-monthly, monthly, or another available option. Pay frequency matters because federal withholding is calculated by annualizing the pay period amount, applying the withholding method, and converting the result back to each paycheck.

- Enter your filing status. Choose the filing status that matches your Form W-4, such as single, married filing jointly, or head of household. Filing status changes the withholding table used for the estimate.

- Add W-4 details. Enter Step 2 checkbox status, Step 3 credits, Step 4(a) other income, Step 4(b) deductions, and Step 4(c) extra withholding if they apply to your current W-4. These fields help the federal withholding calculator give a closer estimate.

- Enter deductions separately. Put pre-tax deductions in the pre-tax field and post-tax deductions in the post-tax field. This separation matters because pre-tax deductions can reduce taxable wages before some taxes are applied, while post-tax deductions reduce only your final take-home pay.

- Add state and local tax estimates. Enter a state tax percentage and local tax percentage when you know the rates or want a practical payroll estimate. Enter 0 when your location has no state or local income tax withholding, or when you want to focus only on federal payroll taxes.

- Use year-to-date wage fields when needed. Add year-to-date Social Security wages and Medicare wages if you are a high earner, recently changed jobs, or want more accurate Social Security and Additional Medicare results.

- Review the breakdown. Click calculate to see gross pay, taxable pay, federal withholding, Social Security, Medicare, estimated state tax, estimated local tax, deductions, and net pay. Use the CSV or PDF export if you need a record of the result.

2026 Payroll Tax Rates and Rules Table

The calculator uses federal payroll rules for 2026 and lets you enter custom state and local rates. Federal withholding uses the IRS Publication 15-T percentage method. Employee Social Security tax is 6.2% up to the 2026 wage base. Employee Medicare tax is 1.45% with no annual cap. Additional Medicare withholding is 0.9% once wages paid by an employer exceed the required threshold. State and local payroll taxes are entered manually because withholding rules vary by state, city, county, school district, and employee situation.

| Payroll item | 2026 rule used | How it affects your paycheck |

|---|---|---|

| Federal income tax withholding | IRS Publication 15-T 2026 percentage method | Uses pay frequency, taxable wages, filing status, W-4 Step 2, credits, deductions, other income, and extra withholding. |

| Form W-4 filing status | Single, married filing jointly, or head of household | Changes the federal withholding table used for the pay period estimate. |

| W-4 Step 2 checkbox | Used for multiple jobs or working spouse situations | Can increase withholding because the job is treated under the multiple jobs adjustment. |

| W-4 Step 3 credits | Annual credit amount entered by employee | Reduces estimated annual withholding before it is divided by pay periods. |

| W-4 Step 4(a) other income | Annual non-job income entered by employee | Can increase federal withholding to cover income not otherwise withheld. |

| W-4 Step 4(b) deductions | Annual deduction amount entered by employee | Can reduce withholding when expected deductions exceed the standard amount built into the method. |

| W-4 Step 4(c) extra withholding | Extra dollar amount per paycheck | Added to each paycheck after the basic federal withholding estimate. |

| Social Security tax | 6.2% employee rate up to the 2026 wage base of $184,500 | Applies only until taxable Social Security wages for the year reach the wage base. |

| Medicare tax | 1.45% employee rate | Applies to covered Medicare wages with no annual wage cap. |

| Additional Medicare Tax | 0.9% employee withholding after wages paid by an employer exceed $200,000 | Can apply during the pay period where Medicare wages from that employer pass the threshold. |

| State tax | Custom percentage input | Lets you estimate state withholding without relying on one national table. |

| Local tax | Custom percentage input | Lets you include city, county, school district, or other local wage tax estimates. |

| Pre-tax deductions | User-entered amount | May reduce taxable wages before selected payroll taxes depending on the deduction type and plan. |

| Post-tax deductions | User-entered amount | Subtracted after taxes and reduce the final net paycheck amount. |

| Net pay | Final estimated take-home pay | Gross pay minus taxes and deductions. |

Official source links: IRS Publication 15-T, IRS Topic 751, SSA contribution and benefit base, and IRS Form W-4 information.

Worked Examples

Assume an employee earns a $72,800 annual salary and is paid biweekly. The annual salary is divided by 26 pay periods, so gross pay is $2,800 per paycheck. If the employee has $150 in pre-tax deductions, the first step is to subtract that amount from gross pay for the deductions that qualify for pre-tax treatment. The calculator then estimates federal withholding using filing status, pay frequency, and W-4 entries. It also calculates Social Security at 6.2% up to the 2026 wage base, Medicare at 1.45%, estimated state tax, estimated local tax, and post-tax deductions. The result is the estimated net pay for that biweekly paycheck.

Assume an hourly employee earns $25 per hour, works 40 regular hours, and works 6 overtime hours at 1.5 times pay. Regular wages are 40 x $25, or $1,000. Overtime wages are 6 x $37.50, or $225. Gross pay is $1,225 before taxes and deductions. The hourly paycheck calculator uses that gross amount, subtracts any pre-tax deductions, then estimates federal income tax withholding, Social Security, Medicare, state tax, local tax, and post-tax deductions. This helps the employee see the take-home value of overtime, not just the gross overtime amount.

Assume an employee already has $183,800 of year-to-date Social Security wages before the current paycheck. The 2026 Social Security wage base is $184,500, so only $700 remains subject to Social Security tax before the cap is reached. If the current paycheck has $3,000 of Social Security taxable wages, Social Security applies to $700, not the full $3,000. Medicare still applies to all covered Medicare wages because Medicare has no wage cap. This is why the year-to-date field is important in a 2026 pay stub calculator.

Assume a married employee is paid semi-monthly and enters annual dependent credits on Form W-4 Step 3. Those credits reduce the annual federal withholding estimate before it is divided by 24 pay periods. If the employee also enters $50 on Step 4(c), the calculator adds $50 of extra federal withholding to each paycheck. This combination can happen when a household qualifies for credits but still wants additional withholding to avoid a tax balance due. The paycheck calculator keeps these W-4 entries separate so the payroll tax estimate is easier to review.

These examples are simplified so the paycheck flow is easy to follow. Real payroll may include cafeteria plan rules, wage garnishments, pretax retirement contributions, Roth contributions, supplemental wages, state disability insurance, unemployment-related employee taxes in some states, city taxes, local school taxes, and employer-specific benefit rules. Use the result as a planning estimate and compare it with your official pay stub.

Quick Reference Table for Pay Stub Terms

| Term | Meaning for paycheck calculation |

|---|---|

| Gross pay | Total earnings before taxes and deductions. |

| Net pay | Take-home pay after taxes and deductions. |

| Pay frequency | How often wages are paid, such as weekly, biweekly, semi-monthly, or monthly. |

| Federal withholding | Income tax withheld from wages based on IRS rules and Form W-4. |

| FICA | Payroll taxes for Social Security and Medicare. |

| Social Security tax | Employee payroll tax applied up to the annual wage base. |

| Medicare tax | Employee payroll tax applied to covered Medicare wages with no cap. |

| Additional Medicare Tax | Extra Medicare withholding for higher wages paid by an employer. |

| Form W-4 | Employee withholding certificate used to guide federal income tax withholding. |

| Step 2 checkbox | W-4 setting for multiple jobs or working spouse situations. |

| Step 3 credits | Annual credits entered on W-4, often for dependents. |

| Step 4(a) | Other income entered on W-4 to increase withholding. |

| Step 4(b) | Deductions entered on W-4 to reduce withholding. |

| Step 4(c) | Extra withholding requested per paycheck. |

| Pre-tax deduction | Deduction that may reduce taxable wages before selected taxes. |

| Post-tax deduction | Deduction taken after payroll taxes are calculated. |

| YTD wages | Year-to-date wages already paid during the calendar year. |

| Taxable wage base | Maximum annual wage amount subject to a specific tax, such as Social Security. |

| State tax estimate | User-entered estimate for state income tax withholding. |

| Local tax estimate | User-entered estimate for city, county, or district wage tax. |

Edge Cases and Exemptions

Paycheck estimates can change when a worker has special payroll conditions. The most common edge case is the Social Security wage base. Once an employee reaches the annual Social Security taxable maximum, Social Security tax stops for the rest of that calendar year for that employer's payroll. Another common edge case is Additional Medicare Tax. Medicare has no annual wage cap, and employers must withhold the extra 0.9% Additional Medicare Tax when wages paid by that employer exceed the federal withholding threshold.

Pre-tax deductions are another area where results may differ from a real pay stub. A traditional 401(k) contribution may reduce federal income tax wages but not necessarily Social Security or Medicare wages. Health insurance, HSA, FSA, and cafeteria plan deductions can have different tax treatment depending on the plan. Roth 401(k) contributions are normally post-tax for federal income tax purposes, so they usually reduce net pay after tax rather than reducing current taxable wages. Garnishments, union dues, after-tax insurance, and charitable payroll deductions are also typically treated differently from pre-tax benefits.

State and local withholding can also create differences. Some states have no state income tax. Some states use flat payroll withholding. Others use detailed tables, allowances, credits, local taxes, disability taxes, family leave taxes, or special wage bases. Cities and school districts may also withhold wage taxes. This calculator includes state and local percentage fields for practical planning, but your employer's payroll software may use a more detailed state-specific method.

When and How to Act

Use this paycheck calculator before making payroll decisions, not only after payday. If your expected net pay looks too low, review your gross pay, hours, overtime, benefit deductions, and W-4 inputs. If federal withholding looks too high or too low, compare your current Form W-4 with your household situation. A life change such as marriage, divorce, a new child, a second job, spouse employment, large side income, or major deductions can change how much should be withheld from each paycheck.

If you want more money in each paycheck, reducing voluntary deductions or updating W-4 entries may increase net pay, but it can also reduce retirement savings or increase tax due at filing. If you often owe tax when filing, adding extra withholding on Form W-4 Step 4(c) can spread the cost across paychecks. If you usually receive a large refund, reviewing credits and deductions on Form W-4 may help you keep more money during the year. Employees should submit a new Form W-4 to their employer when they want payroll withholding changed.

For budgeting, run the calculator for your regular paycheck and for any expected overtime or bonus period. For job offers, compare the same pay frequency and deduction assumptions across offers. For high earners, update year-to-date wages during the year so the calculator can handle the Social Security wage base and Additional Medicare rules more accurately. For official records, rely on your employer pay stub, year-end Form W-2, and tax filing documents.

Frequently Asked Questions

Start with gross pay, subtract eligible pre-tax deductions, calculate federal income tax withholding using IRS Publication 15-T and your W-4 details, calculate Social Security and Medicare, add any state and local withholding estimates, subtract post-tax deductions, and the remaining amount is estimated net pay.

Gross pay is your total earnings before payroll deductions. Net pay is the amount you take home after federal withholding, FICA taxes, state and local estimates, benefit deductions, and other payroll deductions are subtracted.

It works as both. A paycheck calculator estimates take-home pay, while a pay stub calculator shows the line-by-line deduction breakdown that explains how gross pay becomes net pay.

Yes. The calculator estimates federal income tax withholding using 2026 IRS Publication 15-T style inputs, including filing status, pay frequency, W-4 Step 2, credits, other income, deductions, and extra withholding.

FICA is the payroll tax system that funds Social Security and Medicare. Employees generally pay Social Security tax up to the annual wage base and Medicare tax on covered Medicare wages. Employers also pay matching amounts, but the employee pay stub usually shows the employee portion.

The 2026 Social Security wage base is $184,500. Employee Social Security tax applies to covered wages up to that amount. Wages above the annual wage base are not subject to employee Social Security tax, but Medicare tax can still apply.

No. Medicare tax does not have an annual wage cap. Employee Medicare tax continues on covered wages, and high earners may also have Additional Medicare Tax withheld after wages paid by an employer exceed the required threshold.

Your paycheck may be lower because of federal withholding, Social Security, Medicare, state tax, local tax, health insurance, retirement contributions, HSA or FSA deductions, garnishments, union dues, or extra withholding requested on Form W-4.

A traditional pre-tax 401(k) contribution generally reduces federal income tax wages, but it may not reduce Social Security or Medicare wages. A Roth 401(k) contribution is usually made after tax, so it normally does not reduce current federal taxable wages.

Yes. Select biweekly as the pay frequency and enter your gross pay or hourly details. The calculator will estimate taxes and deductions for one biweekly paycheck and show the expected take-home pay.

Yes, it includes a custom state tax percentage field. This is useful for a planning estimate, but actual state withholding can depend on state forms, credits, exemptions, local rules, reciprocity, and employer payroll settings.

It is designed to provide a strong planning estimate using current federal payroll rules and user-entered state, local, and deduction inputs. Actual pay stubs can differ because employers apply specific payroll systems, benefit rules, state tables, local taxes, garnishments, and employee elections.